With prices continuing to fall, James Walton shows where necessary savings can be made.

Last month, Alan Osborn explored the unprecedented deflation now affecting the food and drink industry.

Last month, Alan Osborn explored the unprecedented deflation now affecting the food and drink industry.

At this time, the situation looks unlikely to change. The CPI measure from the ONS had recorded eight consecutive months of reductions in annual food and drink prices, and far from slowing, the pace of reduction is accelerating1.

Good or bad?

So, is deflation a challenge or an opportunity for businesses?

Often, deflation is negative, since falling prices imply oversupply of goods or weakening of demand in a marketplace. In these cases, deflation is often a symptom of wider economic malaise, rather than the cause.

However, the UK is currently recovering, albeit weakly, with measures of economic health, such as GDP and consumer demand, moving upwards.

The actual drivers of food and drink deflation are well understood and are not, in themselves, particularly malign, at least from the viewpoint of the total economy. These include:

- Competitive activity.

- Currency effects making imports cheaper.

- Good harvests for key foodstuffs.

- Falling energy costs.

Whatever the causes – and however long they last – deflation is giving business leaders in food and drink serious headaches. Management challenges associated with deflation include:

- Commoditisation of products.

- Difficulty achieving performance targets, such as growth and labour productivity.

- Difficulty paying off credit.

Deflation is not a process businesses can opt out of – in any market there is only one ‘correct’ price for a product or service: the lowest available.

Wholesalers will inevitably be affected by deflation and, like every other business in the supply chain, they will be looking for savings that will allow them to remain competitive and profitable.

Fuel cost:

Fuel and transport savings are obvious areas to explore. Falling fuel prices naturally create savings for wholesalers, especially delivered wholesalers.

There are many variables, including vehicle type and annual mileage, but fuel accounts for 20-36% of the cost of operating a goods vehicle in the UK2. So, a 5% reduction in the price of fuel will result in a 1% reduction in transport costs – possibly more. This is good news, although savings may be short-lived, as global fuel prices could rebound.

More ominously, fuel savings for wholesalers may be offset by cost increases elsewhere. If clients demand more flexible service, such as more frequent deliveries, then savings may evaporate – perhaps permanently.

Other opportunities:

Other possible savings are harder to identify. Labour costs in particular may be hard to control – unemployment is falling rapidly and some employers already report difficulty recruiting and retaining staff3,4.

Wages in the UK are expected to rise in the near future, especially for in-demand specialities such as HGV drivers5. Automation in depots and stores may help to offset this, although the initial cost is often high.

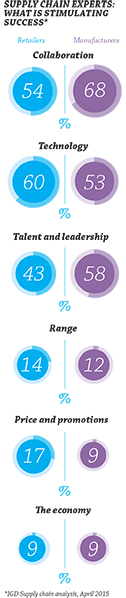

Making the food and drink industry work better is central to IGD’s purpose and we regularly survey senior personnel around the world.

Our latest survey shows that manufacturers and distribution businesses are finding it increasingly difficult to locate additional savings in the supply chain.

This is perhaps to be expected, as the ‘easy wins’ are the first to be realised. Looking ahead, further savings will require more complex activity and advanced operational skills.

Businesses up and down the supply chain may need to work cooperatively to unlock the necessary savings. This in turn implies a need for trust and the equitable sharing of both costs and benefits.

For these reasons, participants in the IGD survey tended to identify ‘soft’ skills such as collaboration and leadership, as key determinants of success in the supply chain.

Big businesses do not have a monopoly on these attributes. Smaller suppliers and wholesalers can therefore look to these skills to help them remain competitive – and relevant – in the current deflationary food and drink market.

Sources:

1ONS measure D7G8, the food and drink annual CPI, for February 2015

2FTA research, October 2014

3ONS measures MGSC and MGSX, unemployment, for December 2014

4Labour Market Outlook Winter 2014-15, CIPD, February 2015

5Economic and Fiscal Outlook, Office for Budget Responsibility, March 2015